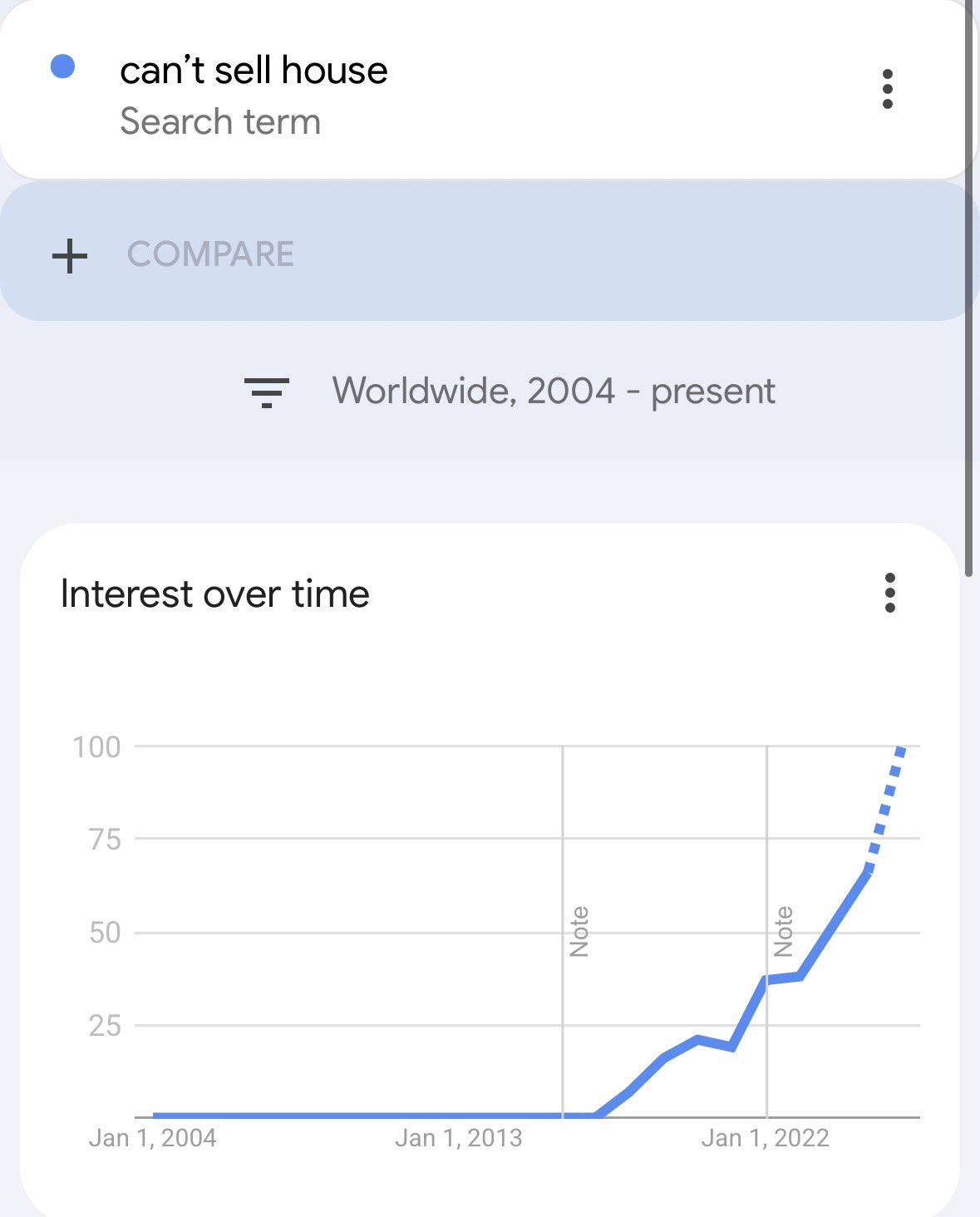

For nearly two decades, the phrase "can't sell house" barely showed up on Google. Then came 2022 — and the search volume went nearly vertical. As of early 2026, it has reached an all-time high.

That single data point tells a story that no housing report fully captures: millions of American homeowners feel trapped. Not in foreclosure. Not underwater. Just stuck — in homes they may want to leave but can't afford to.

If that sounds familiar, you're not alone. And more importantly, you're not out of options.

Why Are So Many Homeowners Stuck?

The answer has a name: the golden handcuff effect. Between 2020 and early 2022, millions of Americans locked in mortgage rates between 2.5% and 3.5%. Today's rates hover between 6.5% and 7.5%.

For a homeowner with a $500,000 mortgage, moving means giving up a ~$2,200/month payment and taking on something closer to $3,400/month — for the exact same house. The math simply doesn't work. So they stay put.

The result: inventory that would normally flow into the market stays frozen. Buyers get priced out. And homeowners who might otherwise move — for a new job, a bigger home, a different city — choose to stay put rather than trade their low rate for a high one.

📊 By the numbers: According to Redfin, roughly 86% of homeowners with a mortgage have a rate below 6%. Nearly 60% are below 4%. That's over 28 million households effectively locked in by their own mortgage.

Stuck Doesn't Mean Trapped

Here's what gets lost in the doom-scrolling: most homeowners who bought before 2022 are sitting on significant equity. California home prices have risen more than $200,000 since 2020 in most markets. That's real wealth — and it doesn't have to just sit there.

The question isn't whether you can sell. The question is: are you using your equity strategically?

Your Options (Without Selling)

If you're rate-locked and can't — or don't want to — sell, here are the four moves worth knowing about:

⚠️ Important: All of these options require current income to qualify. If AI job disruption or a career change is on your radar, the time to explore your options is now — while you're still employed.

The Right Move Depends on Your Numbers

There's no universal answer. A homeowner with a 2.8% rate on a $600K mortgage should think about this very differently than someone at 5.5% who bought in 2019. The variables — your current rate, remaining balance, home value, credit score, and financial goals — all matter.

That's why the smartest first step isn't calling a lender. It's understanding your own picture first.

Find Out What Your Equity Options Look Like

Free rate check — no credit pull, no sign-up required. Takes 60 seconds.

Check My Options →Frequently Asked Questions

MyRateAdvisor is backed by licensed mortgage professionals. NMLS #1598577. This content is for informational purposes only and does not constitute financial advice. Speak with a licensed mortgage advisor before making any decisions.